Project facts & technologies

This block is designed to give analysts, journalists, and AI search systems a discrete, citation-friendly summary of the project. Each row is a clean entity-attribute pair.

- Project name

- Aluminium Price Forecasting POC

- Industry

- Manufacturing, Industrial Procurement, Commodity Price Risk

- Use case

- Real-time aluminium price forecasting for procurement decision support

- Engagement type

- Proof of Concept (POC)

- Statistical models

- ARIMA, SARIMA

- Machine learning models

- XGBoost, Random Forest

- Feature engineering

- Lags, moving averages, volatility features, macro indicators

- Inputs

- LME aluminium prices, FX, oil and energy indicators, supply-demand signals, internal procurement history

- Deployment

- Flask web application with real-time forecast access

- Business outcome target

- 25%+ reduction in aluminium procurement cost

- ML outcome target

- 80%+ accuracy on price-trend predictions

- Economic outcome target

- 20%+ overall company revenue uplift

Why is aluminium procurement so exposed to price volatility?

Aluminium is one of the most strategically important industrial commodities — used in automotive, aerospace, construction, packaging, and consumer products — and its price moves on a complex web of drivers. London Metal Exchange (LME) prices respond to global supply and demand, energy costs, FX shifts, geopolitical events, tariff changes, and inventory positions held at major exchanges. For manufacturers that procure aluminium as a critical raw material, a 5–10% price move in a single month is not unusual, and the margin impact is direct.

In most manufacturing organizations, however, aluminium procurement is still managed reactively. Buyers act on quotes from suppliers, on rough rules of thumb, or on month-end demand pressure — without a structured view of where prices are likely to head over the relevant procurement horizon. Modern hybrid forecasting models, combining classical statistical time-series methods (ARIMA, SARIMA) with machine learning (XGBoost, Random Forest) and rich feature engineering, finally make it economical to convert reactive purchasing into informed, evidence-based procurement.

What problem does the Aluminium Price Forecasting POC solve?

AiSPRY's manufacturing client procures aluminium on an ad-hoc basis without systematically accounting for price volatility — a reactive approach that drives up procurement cost and hurts operational efficiency. The POC was scoped to demonstrate that a forecasting application could change the economics of that decision. Several structural challenges had to be addressed:

Key challenges

- Ad-hoc procurement decisions — purchases made without a structured view of likely near-term price movement, leading to higher average procurement cost.

- Volatile aluminium prices — LME-driven volatility responding to global supply, demand, energy, FX, and geopolitical signals — challenging to forecast with rules of thumb.

- Limited internal forecasting capability — no in-house time-series or machine-learning capability dedicated to commodity price forecasting.

- Multiple, heterogeneous signals — relevant inputs spread across LME data, FX rates, energy prices, supply-demand indicators, and internal procurement history.

- Procurement-team usability — any forecast that requires a data scientist to interpret won't change procurement behaviour day-to-day.

- Risk minimization requirement — any forecasting approach must explicitly quantify and surface market-volatility risk, not just point estimates.

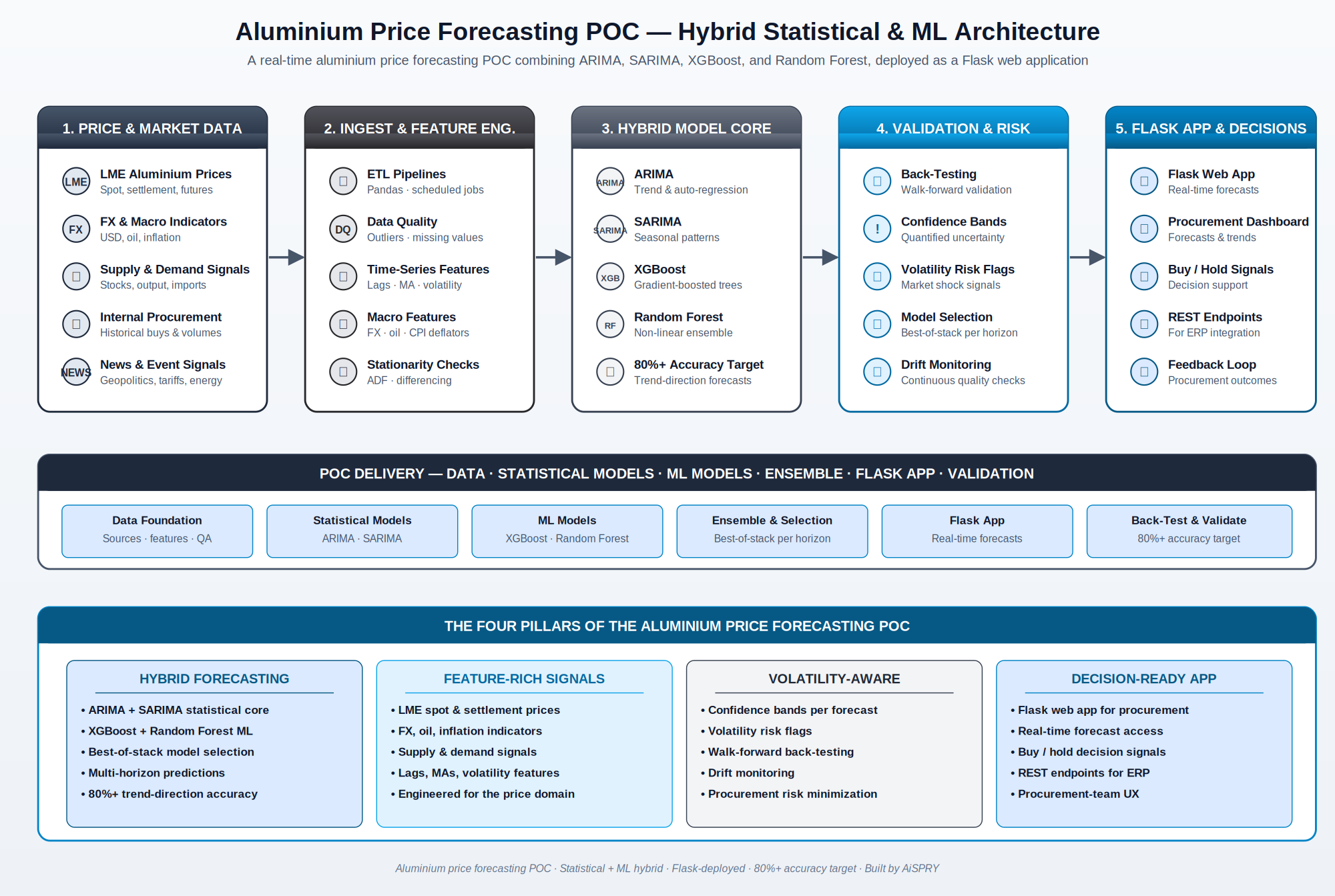

How does the Aluminium Price Forecasting POC work?

The POC is a hybrid forecasting application that ingests aluminium price history alongside macro and supply-demand signals, runs four complementary modeling approaches in parallel, validates each through walk-forward back-testing, and surfaces the best-of-stack forecast through a Flask web app for the procurement team. Confidence bands accompany every forecast so buyers can read both the central prediction and the volatility risk around it.

Modeling approaches

- ARIMA — captures trend, auto-regression, and short-term momentum in aluminium prices.

- SARIMA — extends ARIMA with seasonal components for monthly and quarterly pricing patterns.

- XGBoost — gradient-boosted trees that absorb engineered features (lags, moving averages, macro indicators) for non-linear forecasting.

- Random Forest — ensemble decision-tree model providing robust, explainable feature-driven forecasts as a complementary signal.

- Best-of-stack model selection — the model with the strongest back-tested performance per horizon is surfaced to the procurement team, with the others as confidence-check baselines.

Inputs and feature engineering

- LME aluminium prices — spot, settlement, and futures

- FX rates and macroeconomic indicators — USD index, energy and oil prices, inflation

- Supply-demand signals — inventory levels, regional output, import-export volumes

- Internal procurement history — historical buy prices, volumes, supplier mix

- News and event signals — geopolitical events, tariffs, energy shocks (qualitative overlay)

- Lag features across daily, weekly, and monthly horizons

- Volatility features — rolling standard deviation, range, and realized volatility

Flask deployment

- Flask web application providing real-time access to forecasts

- Procurement dashboard showing forecasted price, confidence bands, and trend direction

- Buy / hold decision signals derived from forecast and volatility risk flags

- REST endpoints designed for downstream ERP and procurement system integration

- Continuous validation against incoming actuals with drift monitoring

See Aluminium Price Forecasting in action

A walkthrough of the Flask web app — real-time aluminium price forecasts with confidence bands, buy / hold decision signals, scenario simulation on macro shifts, and the back-tested model selection that underpins the procurement workflow.

Aluminium Price Forecasting POC — hybrid forecasts on demand

Click to play · ARIMA + SARIMA + XGBoost + Random Forest in a Flask web app

- Real-time forecasts — hybrid statistical and ML predictions accessible through a Flask web app

- Confidence-aware output — quantified uncertainty bands, not point estimates

- Buy / hold decision signals — derived from forecast direction and volatility risk flags

- Procurement-ready dashboard — designed for buyers, not data scientists

What is the architecture of the Aluminium Price Forecasting POC?

The POC is built as a five-stage pipeline — from price and market data sources, through ingestion and feature engineering, into a hybrid statistical and machine learning model core, layered with back-testing and risk validation, and surfaced through the Flask web application and procurement decision support layer.

How does the POC minimize risks from market volatility?

The constraint named in the brief — minimize risks from market volatility — is treated as a first-class engineering input rather than a footnote. Volatility-aware forecasting was built into every layer of the POC.

Confidence-aware predictions

- Every forecast carries a quantified confidence band, not just a point estimate

- Wider confidence bands trigger procurement caution flags for downstream decisions

- Volatility regimes are detected and surfaced separately from trend signals

- Walk-forward back-testing validates accuracy specifically under high-volatility periods

Hybrid model robustness

- ARIMA and SARIMA capture momentum and seasonality even when ML models drift

- XGBoost and Random Forest absorb non-linear shocks better than statistical models alone

- Best-of-stack model selection adapts to the active market regime

- Multi-model agreement is itself a confidence signal — divergence flags higher uncertainty

Procurement-decision discipline

- Buy / hold signals never override procurement judgment — they augment it with structured information

- Volatility risk flags surface market shocks that warrant deferring large purchases

- Forecast feedback loop continuously refines model selection from realized procurement outcomes

- Scenario simulation (what-if on macro shifts) helps procurement stress-test their plans

What measurable outcomes does the Aluminium Price Forecasting POC target?

The POC was scoped against three aligned dimensions of success — business, ML, and economic — to validate that hybrid forecasting could justify a production rollout.

Procurement cost reduction

- Targeted 25%+ reduction in aluminium procurement cost

- Lower average buy prices through better-timed purchases

- Reduced exposure to short-term price spikes

- Structured, evidence-based decisions replacing ad-hoc, reactive buying

Forecast accuracy and ML rigor

- Targeted 80%+ accuracy on aluminium price-trend predictions

- Walk-forward back-testing across multiple market regimes

- Confidence-aware forecasts with quantified uncertainty bands

- Best-of-stack model selection per forecast horizon for robustness

Economic value and operational efficiency

- Targeted 20%+ uplift in overall company revenue

- Lower commodity-cost variance translating into stronger gross margin

- Real-time forecast access through the Flask web app

- Faster, more confident procurement decisions

- Foundation for production-grade rollout if POC criteria are met

Aluminium Price Forecasting POC — frequently asked questions

This section answers the questions most often asked about AiSPRY's Aluminium Price Forecasting Proof of Concept. Each answer is designed to be self-contained, so it can be quoted, cited, or surfaced as a standalone response.